Imagine two companies making the same profits; even the book value of their assets is similar. Which of them is more successful and heads towards long-term growth? To evaluate the economic side of business, it is necessary to decipher which activities provide flow of money into or out of the company.

🎓 CAFLOU® cash flow academy is brought to you by CAFLOU® - 100% digital cash flow software

Cash flows in a clear table

The income statement (overview of income and expenses) will not be sufficient for the needs of financial management. So, where can we find out how the company manages in the operating and non-operating area, how it finances inventories, fixed assets and what was the source of financing? The answer comes from the cash flow statement. Or it can just be called cash flow. It is a table that tells you where the money comes from, what the company actually uses the money for and why it is lacking money.

With the cash flow statement, you will discover the reasons why the company is insolvent and does not have money to pay for invoices even though it is making profit, or vice versa, how is it possible that the company has enough money even though it is showing loss.

Operating, investment and financial cash flows

In the cash flow statement, classify cash flows according to the use of money, i.e. as the company’s operating, investment and financial activities. Think of them as individual floors. It is useful for financial management, but also for appreciating the economic condition of the company. Does the activity because of which you are in the market bring enough money? The answer is on the operating cash flow line. You can find it in the official statement, which you can generate in the pre-prepared reports of your accounting software. When the value of the operating cash flow is positive, income from sales of goods, products and services covers the company’s common expenses, from the purchase of materials, through the payment of wages and interests, to the income tax. It is information about whether the basic activities of the company are meaningful, i.e. whether they bring money to the company.

The imaginary second floor of cash flow is called investment cash flow. This part of cash flow is intended for the acquisition and sale of machines, production lines, cars, buildings, land, software and other fixed assets. This may also include income from profit shares in property-related companies or interests received from credits, loans and assistance to other companies, as it is also an investment. In case of successful companies, investment cash flow is usually negative. It is a sign that the company wants to keep up with the competition in an ever-changing market environment and invests in the development and renewal of its assets.

Now, let’s ascend to the top floor of cash flow. The third area of income and expenses of the company is financial cash flow. Cash flows related to obtaining or returning business resources are belong there. This means financial resources outside the normal activities of the company, such as those brought by owners and external creditors. In cash flow, this will result in the drawing or repayment of credits, the payment of financial leasing or the payment of profit shares to associates.

💡 Have you already tried CAFLOU® - the 100% digital cash flow software ❓

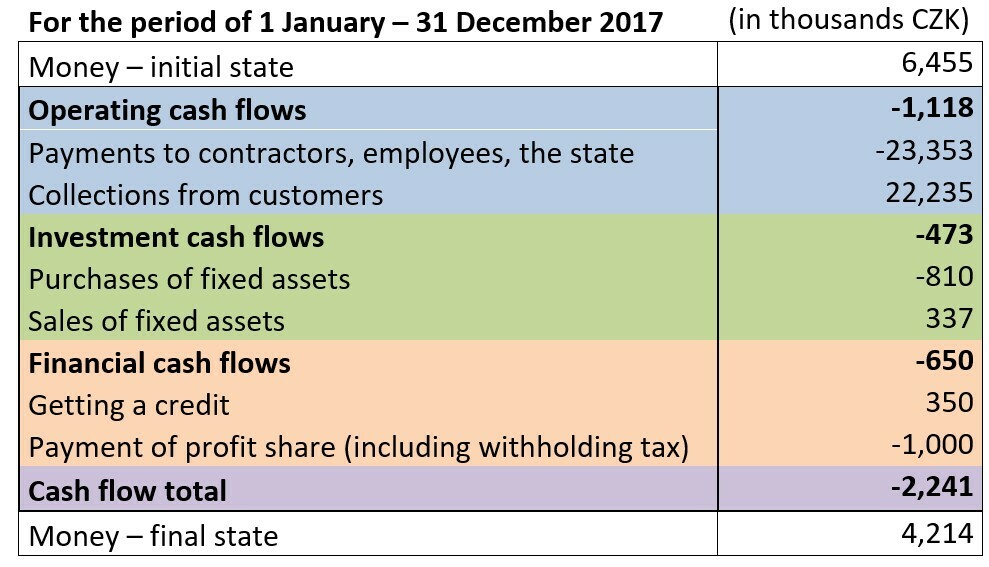

Cash flow statement (example)

The operating cash flow should be clearly positive. This is not the case in the example given. The main activity of the company not only did not bring money to the company in the year 2017, but it also drew more than CZK 1 million from its funds. On the other hand, the company acquired new fixed assets, although it also sold some fixed assets. The statement also shows that the company drew a credit and paid the owners CZK 850 thousand in profit share (the remaining CZK 150 thousand were paid by the company in the form of withholding tax to the state). The total 2017 cash flow is negative. Although the company survived this unfavourable situation with a positive account balance thanks to sufficient initial money reserves, it is clear that it will be able to manage this way only for a few years. How would you like your cash flow to look?

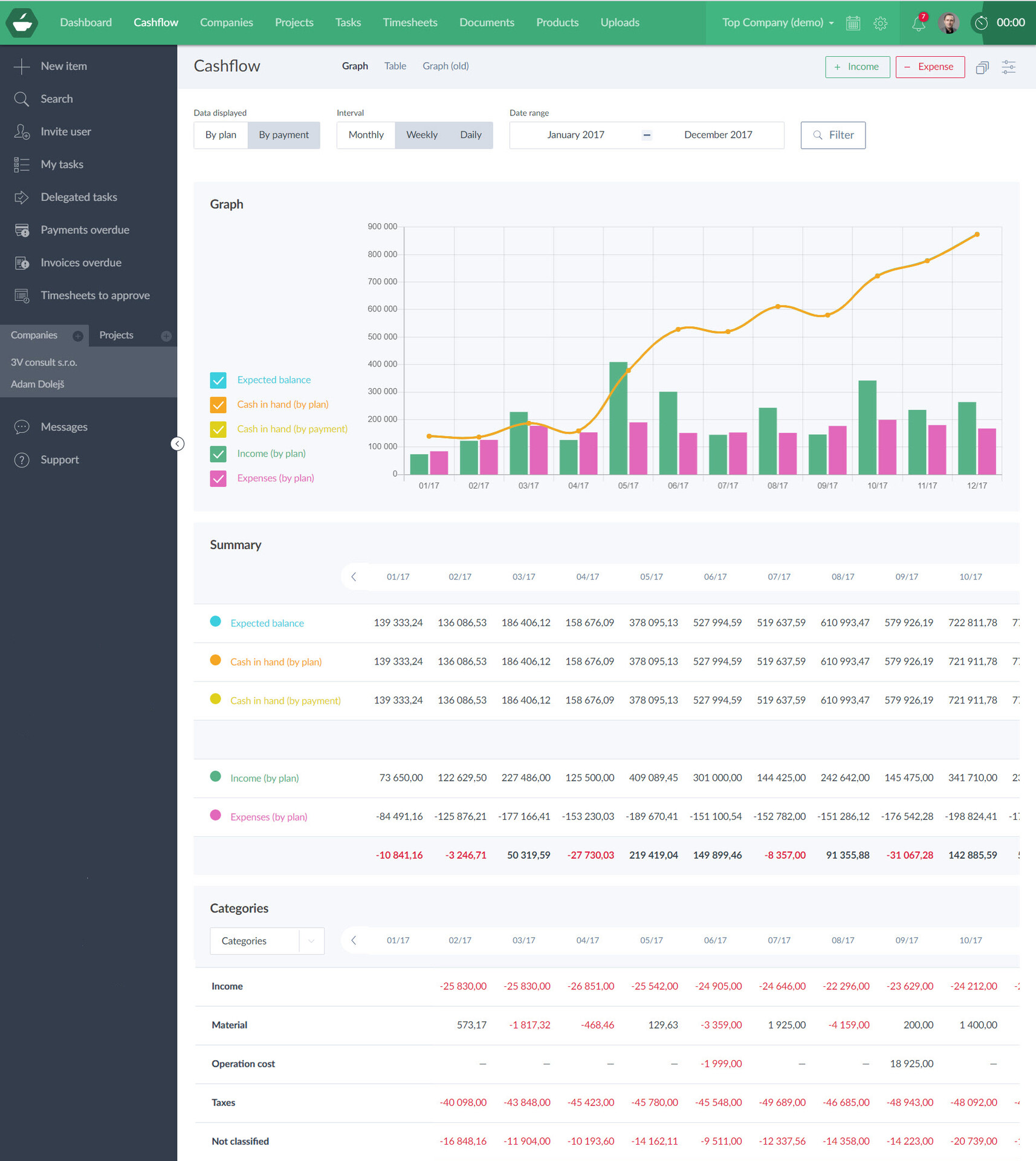

Here is an illustration of similar example with the output from Caflou (see the breakdown for Categories):

<< Back to all articles in Caflou cash flow academy

Article author: Pavlina Vancurova, Ph.D. from ![]()

In cooperation with Pavlina Vancurova, Ph.D., specialist in business economics from consulting firm PADIA, we have prepared the Caflou cash flow academy for you, the aim of which is to help you expand your knowledge in the field of cash flow management in small and medium-sized companies.

In her practice, Pavlina provides economic advice in the area of financial management and setting up controlling in companies of various fields and sizes. In 2011, she co-founded the consulting company PADIA, where she works as a trainer and interim financial director for a number of clients. She also draws on her experience as the executive director of an international consulting firm. She worked as a university teacher and is the author of a number of professional publications.